Market Commentary

There is Always Opportunity

January 2017

"Say goodbye to the Oldies but goodies

‘Cause the good ole days weren’t always good

And tomorrow ain’t as bad as it seems"

- Billy Joel, “Keeping The Faith”

As we write to you on the eve of the 45th President of the United States taking the Oath of Office, many in this country are looking ahead with bewilderment or trepidation that the incoming President will actually keep his campaign promises. The President's supporters, however, are counting on his promise to return this country to some sort of golden era – the "good ole days". For some of us, when Billy Joel was singing Keeping the Faith back in 1983, that was the golden age. Billy Joel, in the early eighties, was reflecting on his own golden age. Today, others may be wondering, "who's Billy Joel?"

Times change and economies (and politics) move in cycles, but there are always areas of opportunity in the vast landscape of modern markets. So that triggers an important question - opportunity for what?

Opportunity for growth. Growth requires taking on some degree of risk, and investors are compensated for that risk only when they are able to buy at the right prices, and hold on through volatility. In the current landscape we see emerging markets as a potential area of opportunity due to recent price pressure, despite some obvious risks that exist for typically export-reliant countries. From Election Day through the end of the year, the emerging market index declined by 6.5% on fears of tariffs and protectionist policy. There is a real question of how or if these campaign statements will be carried out, and whether other administration officials may soften the actual policy on these matters. Additionally, the long-term demographic and economic trends in emerging markets provide further evidence for a narrative of continued growth—3 billion people will be entering the middle class1 and $30 trillion of annual consumption by 2025.2

As for US equities, if the Trump administration can thread the needle of lowering corporate and individual taxes alongside some infrastructure stimulus then there could be opportunity there. Due to stretched valuations at present, our models are slightly underweight with our US equity allocation. Nonetheless, our clients retain substantive exposure to this core asset class, and would benefit from a continuation of the current rally.

Opportunity for caution. There are plenty of reasons to be cautious about the upcoming years, and not all of them have to do with the US political landscape. One recurring theme that we believe will continue to shape politics and policy is the anti-globalization populist movements that propelled both Brexit and our own election results. The EU has shown signs of fraying at the edges, and 2017 will present further tests of EU cohesion. The US market – post election – has reacted to the incoming administration with a rally in stocks; counting on accelerating growth fueled by lower taxes, less regulatory oversight, and fiscal stimulus in the form of massive infrastructure spending. Unfortunately, stimulus may not be enough, in particular, due to concerns related to demographic limitations on GDP growth.

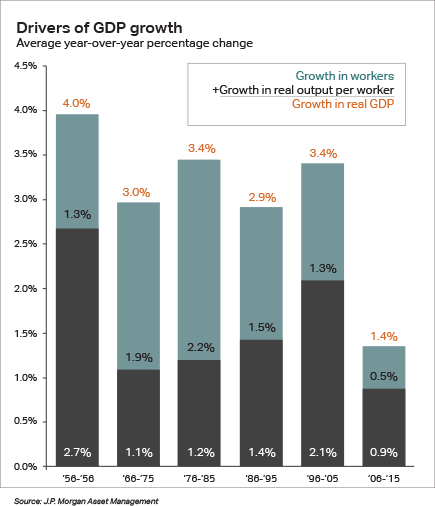

The chart to the right breaks down the components of GDP growth over the last six decades. The two components of GDP growth are the growth in the size of the workforce plus the growth in the output productivity of workers. The past decade has not been generous on either front. Labor force expansion has slowed to an average of 0.5% per year, and productivity growth has declined to just 0.9%. Both are the lowest average readings in at least six decades: fuel for a populist fire, indeed.

Prospects for accelerating growth, the kind that the market seems to be pricing into the recent rally, may be difficult to achieve, even with massive fiscal stimulus. The forecasted annual growth rate for the working age population for the decade from 2015 to 2024 is a scant 0.4%3 Long-term growth expectations are always tricky, but demographic trends have a long arc.

The other component is productivity growth. Prior to the past decade, productivity growth ranged from a low of 1.1% per year to a high of 2.7% per year, with an average rate of 1.7% across the 50-year period. If we then construct a GDP growth outlook by combining the 0.4% workforce growth rate with the half-century productivity growth rate of 1.7%, that barely gets the economy to a 2% clip, substantially short of the post-war average of 3.2%.

These demographic challenges added to valuation concerns gives us pause about near-term growth in the US, and we’ll be patient as we wait for opportunities.

Opportunity for impact. There are an increasing number of social impact funds and private investments that our clients are taking advantage of to have a positive impact on their world. These range from environmental impact to fair labor practices to diversity in company leadership and responsible governance. This is one way for interested clients and citizens to vote with their dollars and have an impact on their world.

We welcome conversations with each of our clients about which of these three types of opportunity — growth, caution, or impact — should be a primary driver in their portfolio and in their life, and which should play a supporting role. And, as always, we continue to be grateful for the trust that our clients put in our team, and we will continue to work diligently to navigate your portfolios toward ports of opportunity.

This is a general assessment of client portfolios and does not reflect the specific circumstance of every client.

1. Ernst & Young, “Innovating for the next three billion”, 2011

2. McKinsey, August 2012, “Winning the $30 trillion Decathlon”

3. J.P. Morgan Asset Management; 1Q 2017 Guide to the Markets

« Previous Article | Next Article »